The Pakistani government in fiscal year budget 2025-26 has decided to initially reduce and eventually eliminate tariffs, or tax on imports, on car imports by 2029 which is currently at 40%. This policy may seem as a step toward rationalising trade and increasing accessibility, but it may as well be the government’s recipe for disaster. The policy encourages consumption, crowds out investment and could threaten Pakistan’s already weak stock of national assets such as infrastructure, machinery and tools that help businesses make future production larger.

Tariff removal will boost consumption; cheaper autos will attract Pakistani consumers, who will pay for these imports with their savings as incomes are likely to remain unchanged. This can be explained through the basic consumption equation where economists describe consumption as having two parts: a basic level of spending regardless of income and additional spending that grows as people’s disposable income (income left after taxes) rises. Reduced tariffs encourage both, the baseline spending and the tendency to spend more of each additional rupee of income (this depends on several other factors like inflation, interest rates etc). Hence as consumption in an economy increases disproportionately, especially compared to savings, the balance of the economy can shift. With output stagnant and increased imports, the economy will be at risk of deepening the trade deficit, inhibiting investment and leaving little to no productive resources for government spending G.

So why are low investments a problem? The answer lies in the Solow Growth Model – a growth model that focuses on investment and innovation – tells us that long-term economic growth depends on building national assets and technological progress and not just consumer demand. Since imported cars are not resources that help produce goods and services, they do not raise the capital stock, and hence the total output remains unaffected. Consequently, in Pakistan, as investment in infrastructure and innovation falters, capital accumulation slows down, pulling Pakistan toward a lower long-term level of economic output. It is worth noting that the Solow model predicts economic growth in the very long run, say, for example, 20 to 30 years, therefore, we cannot confidently base our analysis solely on Solow. Nevertheless, the model helps us understand Pakistan’s economic landscape in terms of consumption and investment.

The global economy is riddled with examples of both consumption and the lack thereof. Before the 2008 global financial crisis, American consumers took massive debt to purchase houses, encouraged by cheap credit and subprime mortgages. As borrowers defaulted en masse, panic settled in and banks began declaring bankruptcy, leading a period where banks stopped lending money globally.

In contrast, Japan cautions against abject saving behaviour. After its bubble burst in the 1990s, Japanese consumers lost immense private wealth and resorted to precautionary saving where firms and households hoarded cash instead of investing due to fear or uncertainty. This resulted in a puzzling situation where the financial system was unable to convert savings into productive investments like businesses or infrastructure. Even as the government introduced near zero interest rates as a last resort to induce demand, growth remained sluggish, and Japan entered the lost decades of economic stagnation.

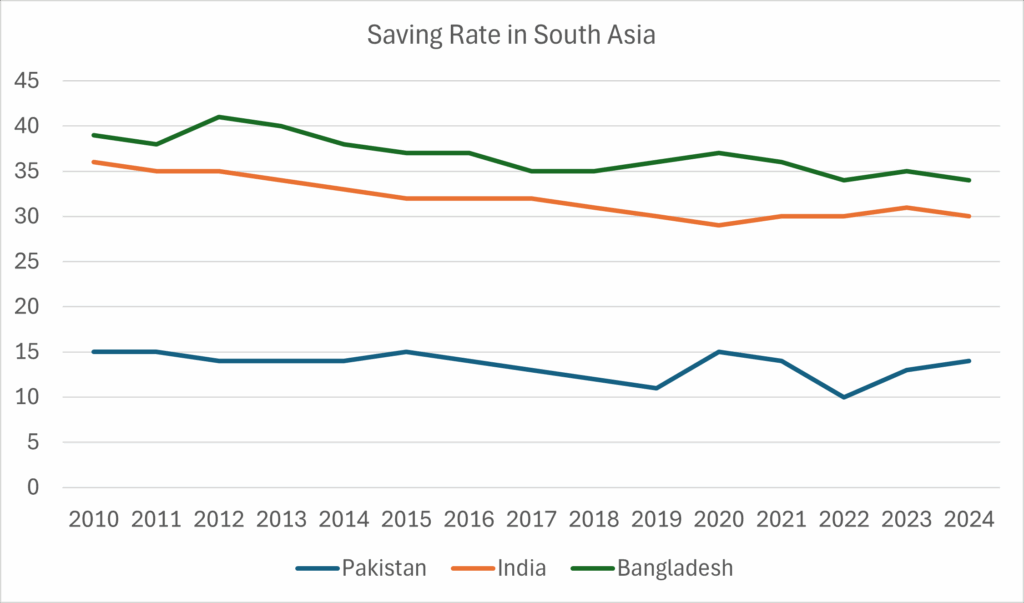

These examples are crucial for understanding Pakistan’s precarious position. Unlike Japan, it doesn’t suffer from excessive saving, but like the USA, it faces an unsustainable consumption problem – without the institutional strength to manage the consequences. This is not to say that Pakistan is as consumption oriented as the USA, but the nature of its consumption is deeply problematic. In the United States, since almost all consumption channels are formal, money circulates back into the financial system – something not true for Pakistan. Here, consumption is largely undocumented, as purchases are made in cash without receipts. Trade deficits escalate because consumption is mostly import driven and fails to build domestic industries capable of production and export. Weak tax laws mean much of the economic activity doesn’t contribute to public revenue. Moreover, a significant portion of expenditure is unproductive, as consumers are predisposed to flashy stunts and throw away lifetime savings on luxury goods, real estate, and lavish weddings instead of making investments that generate future income. Pakistan’s saving rate, averaged at around 13-14%, excludes much of the informal hoarding of cash that sits idly in lockers or stays hidden under mattresses rather than supporting capital accumulation. Hence, Pakistan’s condition may be worse; the consumption it encourages fails to feed into the formal economy.

However, over protectionism has its own challenges, especially in the auto sector, where it has, for decades, limited quality and raised prices for outdated vehicles. Introduced in the 1990s, the policy was aimed at integrating local manufacturers into global value chains; this has failed, and such policies have now become obsolete. Opening protected markets encourages competition and incentivises local producers to innovate and improve product quality. Nevertheless, imports cannot be allowed to soar unchecked – particularly in an import driven economy like Pakistan where imports risk further destabilising the current account and deepening the trade deficit.

The government, instead of focusing on short term goal, such as boosting consumer satisfaction through cuts in import tariffs, should redirect its efforts toward expanding the productive base and growing capital through public development projects. Furthermore, altering public behaviour with relation to saving and investment, albeit challenging, is necessary. Improving financial literacy, restoring trust in banks and digitizing transactions are some of the measures that can make it less challenging.

The tariffs reforms, although politically appealing, seem short-sighted. Encouraging consumption at the expense of investment risks soaring trade deficit. Without reasonable reallocation of saving and investment, there is a good chance the economy will progress toward stagnation.

References

- World Bank. (n.d.) Net general government interest payments (% of revenue) — Bangladesh, India, Pakistan. Retrieved October 15, 2025, from (http://bit.ly/47arg6C)

- Mustafa, G., & Hussain, S. (2023) What are the factors making Pakistan’s exports stagnant? Insight from literature review [Knowledge Brief No. 99] Pakistan Institute of Development Economics. (http://bit.ly/4nKGhTC)

The author is an Undergraduate Student at School of Social Sciences and Humanities (S3H), National University of Sciences and Technology (NUST). She can be reached at [email protected].

![]()